Compass Investors

The Problem Is...

...Traditional (aka, formulaic or pie-chart) investment

strategies are not aligned with the

realities of an increasing

life expectancy.

...Traditional (aka, formulaic or pie-chart) investment

strategies are not aligned with the

realities of an increasing

life expectancy.

Increasing Life Expectancy. People are living longer and therefore requiring a larger nest egg to support the potential of several decades of retirement.

Inflation. Living longer means inflation—even at current levels—will take a large bite out of your purchasing power. And, despite historically low inflation, essentials such as energy, health care, education and other basics are rising faster than ever.

The Unexpected. The longer you live, the more likely you are to become a casualty of factors beyond your control. For example: parents may require additional care in their later years, grown children may come back to live with parents, family members may experience personal health challenges, there may be further uncertainty about the viability of entitlement programs such as social security and pensions, etc.

Just putting more money away—without an accompanying increase in investment return—will likely leave you unable to meet these challenges.

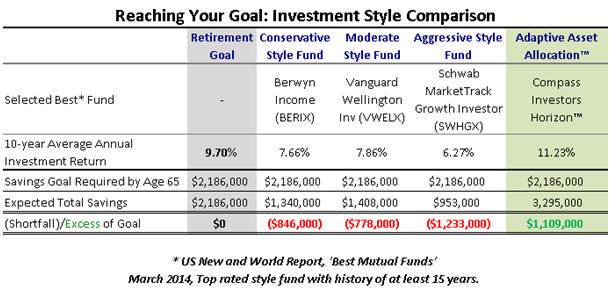

Consider a 30-year old making $40,000 with retirement savings of $37,000 (the national average according to Forbes). After adjusting for inflation during her 35-year remaining work career, in order to insure she does not outlive her money, her necessary nest egg goal is $2.2 million. Why this goal? With a 9% yearly contribution rate, a minimum investment return of 9.7% would enable her to reach her goal.

Let's look at the results of using the best formulaic mutual fund (as rated in 2013 by US News and World Report) with at least a 15-year track record from each of 3 different investing styles . (Refer to the table below.)

The best investment return of any of the possible fund choices reviewed was only 7.9%. This seemingly small difference, versus her required 9.7% minimum return, would leave our worker nearly $800,000 short of her goal at age 65.

Investment return is the catalyst for growing any portfolio. HORIZONTMs 10-year investment return of 11.2% would provide our retiree $1.1 million above and beyond the goal. Unlike putting away more money that only contributes dollar-for-dollar, a larger investment return offers the potential to multiply each dollar saved 2-3 times—or more—over the long-term.

Can you just save more? Assuming our future retiree was fortunate enough to have selected the best performing investment fund (in this case, the Vanguard Wellington moderate style fund) she would need to contribute 17% (up from 9%) of her salary each year—an 88% increase—in order to reach the same nest egg goal. For most people, such a high contribution rate is unrealistic.

Lower your own lifestyle expectations for retirement

Significantly increase what you contribute every year

Adopt an investment strategy with higher investment returns

If you choose the latter, Compass Investors' HORIZONTM investment service can help.